How banks generate revenue from embedded finance

For community banks, embedded finance is a proven way to grow deposits and generate fee revenue. Learn how it works and how much you could be earning.

The revenue challenge for community banks

Over the last twenty years, banking leaders have faced a new challenge: to continue serving their communities, they must evolve how they reach customers and deliver high-quality financial services.

In the past, banks met their customer’s needs primarily through in-person services at their branches. But today, businesses and individuals increasingly expect to access financial products online. Banks are challenged to adapt their businesses to changing expectations as well as increased competition from non-local banking services.

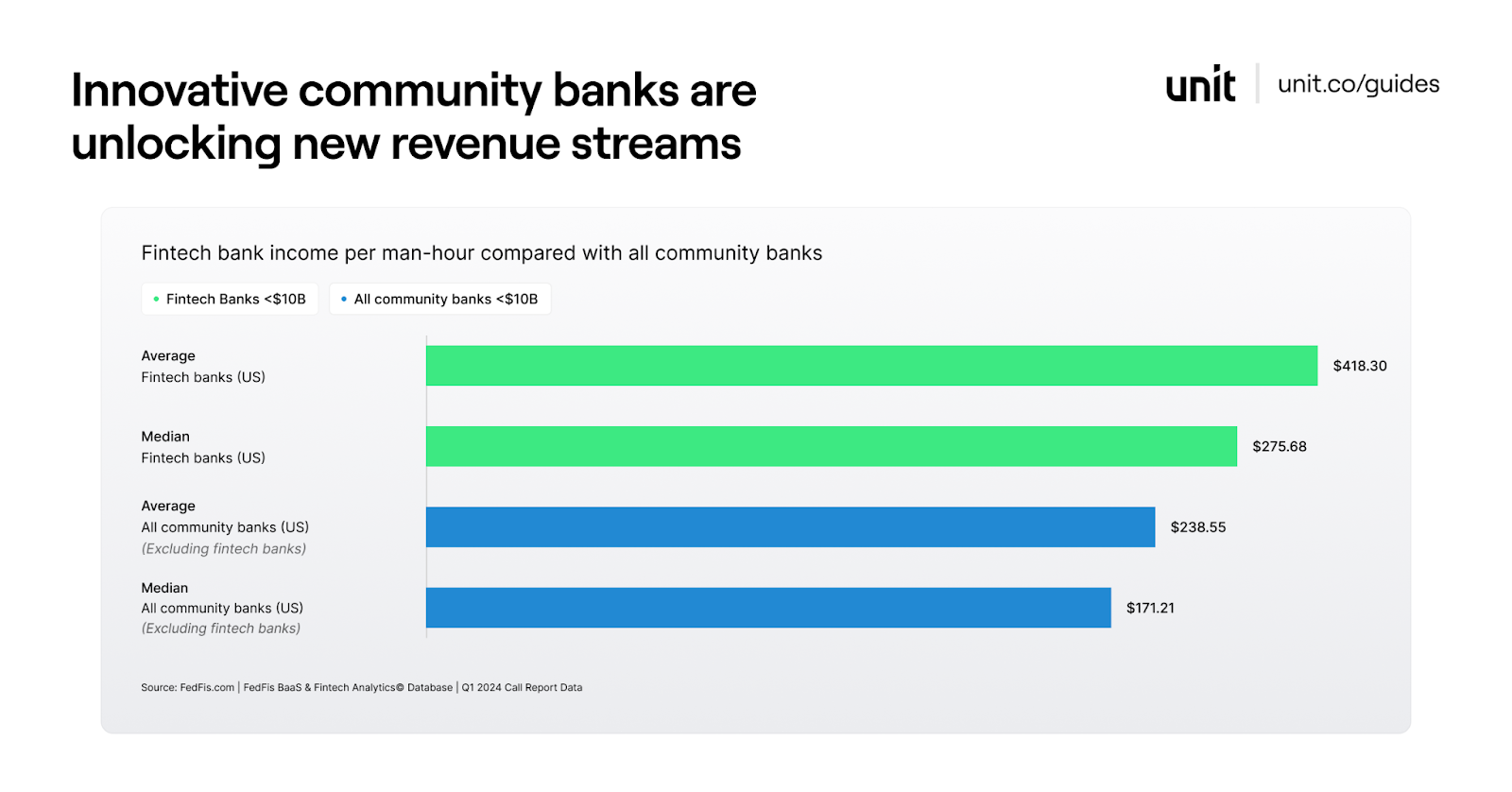

The nation’s largest banks have spent billions of dollars to hire innovation teams and build first-rate digital experiences. But most of America's 4000+ community banks don't have those kinds of resources. Perhaps as a result, they’ve seen their share of the US banking market decline by 50% over the last twenty years.

Fortunately, banks don’t need to spend billions in order to offer a first-rate digital experience. Embedded finance—also known as banking-as-a-service—has emerged as a proven way to connect with new communities and grow revenue.

If you’re a banking leader who’s thinking about how to grow revenue and continue serving communities for generations to come, this guide is for you. In it, we’ll discuss:

- How embedded finance generates net interest margin and fee income

- How other community banks have thrived using this approach

- What it takes to get started

How banks generate revenue via embedded finance

Embedded finance is when banks partner with tech companies to offer financial products inside the tech company’s app or website, often using the tech company’s branding.

For banks, it’s a proven way to connect with new types of customers and grow revenue—beyond the communities they’ve traditionally served.

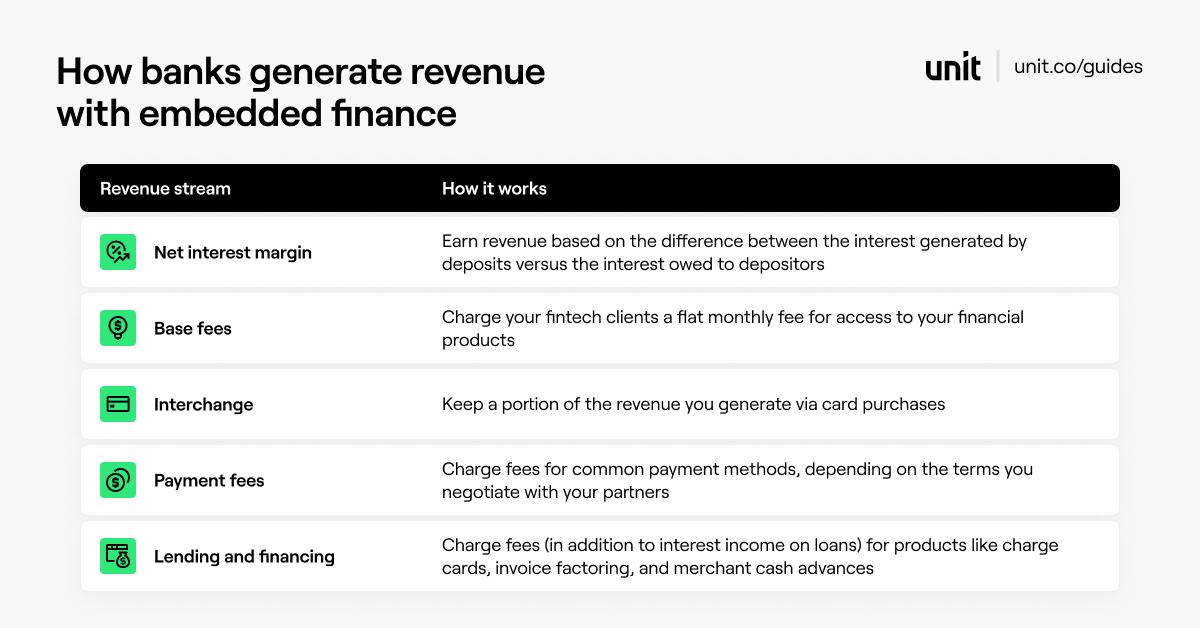

Banks typically think about two types of revenue: net interest margin and fee income. The good news is that embedded finance can help with both.

Net interest margin

Net interest margin is a measure of the return generated by each dollar deposited at the bank: it’s the difference between the return generated by certain assets and the interest owed on the deposits supporting them.

For most community banks, this return comprises the majority of their revenue.

Embedded finance enables banks to generate new revenue by serving customers outside your geographic community. By bringing in new deposits via digital channels, you can generate safe and strategic deposit growth in line with your risk appetite.

How much can you expect to generate in new customers and new deposits? It depends on your goals and digital strategy. As an example, Unit’s bank customers now serve over 1.5 million end-customers through our platform. Together, they hold more than $1 billion in deposits acquired via embedded finance.

Lending and financing fees are another important component of net interest margin. In addition to interest income on loans, there are additional fee income opportunities associated with financing related products like charge cards, invoice factoring, and merchant cash advances.

Fee income

“Fee income” is a broad category that includes all revenue streams outside of interest (e.g., payment fees, interchange, lending).

Here’s one way to think about it. If net interest margin helps you participate in the growth of your fintech clients, then fee income helps you diversify your revenue streams. After all, net interest margin can fluctuate with macroeconomic cycles and monetary policy.

For many banks, fee income is a great way to diversify revenue. Fees can be fixed or variable, and how much you earn depends on what you negotiate with your program partners. Common fees include:

- Base fees. Banks sometimes charge their fintech clients a flat monthly fee for access to their financial products.

- Interchange. Banks commonly keep a portion of the revenue they generate via card purchases, while dividing the remainder between all parties participating in the program.

- Payment fees. Banks may choose to charge fees for certain payment methods—especially those that provide increased speed or convenience, like wires or same-day ACH. What they earn depends on the terms they negotiate with their partners.

Revenue case study: Thread Bank and Roofstock

Thread Bank is a community bank based in Eastern Tennessee.

Recently, they partnered with Roofstock, a real estate platform that helps investors acquire, manage, and sell rental properties. To help landlords manage their finances, Roofstock offers Stessa, a software tool that landlords use to collect rent, screen tenants, and automate accounting.

Through the partnership, Thread and Stessa’s customers can open as many bank accounts as they need, get dedicated debit cards for each property, and automate rent collection. Transactions are automatically tagged to their respective properties and imported to Stessa Accounting, which simplifies tax prep.

Through the partnership, Thread has onboarded thousands of new business customers and millions of dollars of deposits.

It’s been a win for landlords, for Roofstock—and for Thread Bank. Through the partnership, Thread has onboarded thousands of new business customers and millions of dollars of deposits.

The results have been impressive for Roofstock as well: customers who use Stessa Cash Management accounts are engaging more with the platform and spending more money. In fact, they have a customer lifetime value (LTV) 4x higher than other customers.

“Embedded banking was the natural next step for us,” said Heath Silverman, VP of Retail Product at Roofstock. “It improved the customer experience while unlocking better economics for our business.”

Roofstock is a financial technology company, and is not a bank. Banking services provided by Thread Bank, Member FDIC. The Stessa Cash Management Visa® Debit is issued by Thread Bank pursuant to a license from Visa U.S.A. Inc. and may be used everywhere Visa cards are accepted.

What does it take to get started?

Unit is a financial infrastructure platform. We offer industry-leading technology (software, oversight tools, and more) that helps banks partner with promising tech companies.

To date, we’ve been trusted by seven community banks and hundreds of leading tech companies. Unit’s bank customers get the following benefits:

- Robust new revenue streams. Your Unit partnership will enable you to effectively grow your customer base, increase deposits, and create new sources of revenue.

- Introductions to high-quality tech companies. We’ll introduce you to leading platforms and marketplaces. You’ll choose who you partner with based on your goals, target audiences, and risk appetite. You’ll have a direct contract and communications with each of your program partners.

- Best-in-class technology. For many banks, building your own tech stack is not realistic. With Unit, you can access an array of technology and managed services to help you launch, manage, and oversee digital programs.

- Tech-enabled compliance. We provide the tools and data access you’ll need to effectively oversee your fintech clients, like audit logs, decision workflows, and account controls.

- A roadmap for your digital transformation. Many banks think that their digital transformation will take years to complete. By leveraging our best-in-class APIs and platform, our bank customers are typically able to launch their embedded finance programs in six months or less.

Pursuing an embedded finance strategy is a big decision; it’s important to think through the resources required to go live. We look forward to covering what that takes in a future guide.

If you’re thinking about how much revenue you could generate through an embedded finance program, we’d love to chat. Reach out to banks@unit.co.