What would it look like if Apple built banking?

By banking its users, Apple could drive engagement, retention, and revenue. Learn what that might look like and how Apple could power its banking features.

The best bank account is...an iPhone

(Update: it looks like our prediction was correct! On April 17th, 2023, Apple announced the addition of high-yield savings accounts to its Apple Card product.)

In the 1990s, programmer Jamie Zawinksi (known as jwz) asserted that “every software program attempts to expand until it can read mail. Those that cannot are replaced by those that can.”

If it were written today, the saying might read, “Every app evolves until it can hold money for you.”

There are good reasons for this. By overwhelming margins, Americans—both businesses and consumers—say that money is the most stressful thing in their lives. They’re frustrated with the tools they use to manage their finances, and they’re open to trying new ones.

Apple has an opportunity to become their customers' financial mission control—and transform personal finance while they’re at it.

In the ears of a founder or product manager, that sounds like an opportunity, and many companies have stepped up: Chime, Google, Shopify. They aspire to leverage their existing customer base to increase revenue and retention. And a powerful way to do that is to become their customers’ “financial mission control”—their primary account, the routing hub through which all the money passes.

Apple has a compelling opportunity to do just that—and perhaps transform personal finance while they’re at it. In this article, we’ll consider what a full-featured, consumer-focused banking suite from Apple might look like. In doing so, we’ll answer the following questions:

- Why would Apple’s customers want to adopt their banking features?

- Why would Apple want to get into the banking business?

- What banking features would Apple offer?

- What would Apple’s banking features look like?

- How would Apple power their financial features?

But wait. Didn’t Apple already do this?

You may have noticed that Apple already offers some financial products. Today you can apply for an Apple credit card or spend with an Apple Cash card. So what gives?

- The Apple Card is a credit card offered through a partnership with Goldman Sachs Bank. In other words, Goldman does the underwriting and card issuing so that Apple can focus on other priorities.

- Although the Apple Cash card may look like a debit card, it’s not actually, because it’s not linked to a bank account. It’s a prepaid card that Apple offers through a partnership with Green Dot, another bank known for partnerships.

There’s nothing wrong with these products, but they’re missing a few crucial ingredients: bank accounts, debit cards, ACH payments, and additional financing options.

Without those features, it’s not really accurate to call what Apple offers “banking.” Perhaps more importantly, Apple would be missing an enormous opportunity without them.

A breathless public has greeted the arrival of past Apple products, so expectations for the design of their new debit card would be high.

Here’s why Apple should build banking

First and foremost: banking currently lacks the “magic” that Apple is known for.

These days, it’s hard for a checking account to stand out. Nearly all offer the same core functionalities: the ability to hold a balance and send/receive funds.

That said, we strongly believe that Apple’s checking account could be different. Specifically, its value would lie in the software that surrounds it. Deeply understanding their users through data and building that knowledge into their product are two of Apple’s superpowers, and they will add up to a big advantage when it comes time for Apple to build out their banking suite.

- Best user experience. Apple’s personal computers weren’t the first, but they were the prettiest and the most intuitive to use. By taking the time to deeply understand their customers, Apple could design banking products that delight them by anticipating their needs. This would only be heightened by seamless integrations with other aspects of Apple’s product suite (e.g., Apple Card, Apple Pay, iMessage, iCalendar, Apple Watch).

- Personalized financial advice. If you’re an existing customer, Apple knows a lot about you: things like your schedule, your reading list, your location at any given moment, your sleep patterns, your heart rate, your credit card bill, your taste in music and TV, your search history, and the content of your emails. Imagine how powerful that data could be when helping you make a budget, finance a car, choose an insurance provider, or cancel a forgotten magazine subscription.

By taking the time to deeply understand their customers, Apple could design banking products that delight them by anticipating their needs.

- Most attractive terms. In our experience, consumers tend to switch bank accounts when offered strong incentives (e.g., referral bonuses, lower fees). Apple certainly knows this, as evidenced by the attractive rewards on the Apple Card. In the realm of banking, attractive terms could translate to industry-leading interest rates, “always-free” ATMs, or category-based cashback rewards on debit-card purchases.

- Perks for elite users. Over time, Apple would likely become sophisticated in segmenting users of its banking features. Those who spend more, hold higher cash balances, use more financial features, or remain loyal customers could be rewarded with perks like increased cashback, better interest rates, lower (or no) fees, and increased account limits.

But what’s in it for Apple?

More than most companies, Apple could decide to build just about anything.

To become more valuable to their customers, they could invest in original programming for Apple TV+. They could develop new hardware: things like VR headsets, better batteries, or thinner laptops. In the interest of improving their interactive voice technology, they could lean into machine learning.

So why put banking on the roadmap?

- New revenue streams. Apple already generates revenues from Apple Card. By adding bank accounts and additional financing options, they could begin generating revenue from deposits, interchange fees earned on card transactions, and (perhaps most significantly) personal loans. For a company like Apple, with hundreds of millions of users around the world, that could quickly add up to hundreds of millions of dollars. They could also charge a platform fee or charge a small amount for ACH payments—but we suspect they wouldn’t, as they’d prioritize adoption and long-term engagement.

- Engage and retain. On average, Americans check their bank balances twice a week, and they hold their checking accounts for 16.5 years. Adding banking to their product suite has the potential to supercharge Apple’s already sticky ecosystem.

- In-network payments. For Apple, the payments angle is maybe the most interesting. Today, they rely heavily on card networks (e.g., Visa) to facilitate the exchange of value between stakeholders in their own ecosystem. Imagine what would happen if they shifted to in-network payments: fee-free transfers between Apple bank accounts. In addition to their cost advantage, these payments would be near-instant, rich in context, less vulnerable to fraud, and not subject to traditional banking schedules (i.e., they could take place in the middle of the night during Labor Day weekend). If hundreds of millions of users—both consumers and businesses—began defaulting to these payments, it could change the face of financial services.

In addition to their cost advantage, in-network payments are near-instant, rich in context, less vulnerable to fraud, and not subject to traditional banking schedules.

- Micropayments. Apple’s in-network payments could also open the door to “micropayments:” payments of less than one dollar, sometimes even less than one cent, used to compensate content creators and sellers of (typically digital) micro-goods. Companies have long been trying to crack the code on such payments—to make them make sense, economically—and Apple could be the one that finally accomplishes it.

- Synergies with Apple Card and Apple Pay Later. With its users’ consent, Apple could use cash-flow data from their new banking features to improve their underwriting for Apple Card and Apple Pay Later. Users who initially don’t qualify for these financing options could be coached on how to improve their credit scores. If Apple accounts receive users’ paychecks, Apple could offer users automatic repayment of credit products, leading to fewer defaults and less fraud. Finally, as the total amount of their users' deposits grows, Apple could negotiate better terms with the banks that issue their credit products. Those savings could be passed along to users or kept as additional revenue.

- Business banking. The majority of this post is devoted to consumer banking and individual users. But what if Apple banked the developers who sell apps on the App Store or the musicians who license their music to Apple Music? Taking the idea one step further, what if any company could accept payments with an iPhone and manage their business finances on Apple Wallet? Under this model, Apple would essentially be competing with Square and PayPal—only they’d have a big advantage: everyone’s already using their hardware + software. This represents an enormous business opportunity for Apple, not least because they would be making money on both sides of the transaction between businesses and consumers.

Sumukh Sridhara, Head of Product at AngelList, may have spoken for Apple execs when he said: “Banking makes every single feature we offer more interesting.”

This is what a checking account might look like in Apple Wallet.

What would Apple’s banking suite look like?

Core banking features

In Apple’s banking suite, we expect the following features would be included:

- Interest-earning checking accounts. This is the foundation on which all of Apple’s other banking products would be built: a checking account offered through one or more bank partners, insured by the Federal Deposit Insurance Corporation for up to $250,000, with a unique set of account and routing numbers.

- Direct-deposit switch. If you want to identify someone’s primary financial account, just look at where they receive their paycheck. By that logic, if Apple wants to become their customers’ financial mission control, they should make it ridiculously easy for their customers to switch their direct deposits. Fortunately, there are several software tools that enable just that; Argyle, Pinwheel, and Atomic are a few of our favorites. It may even make sense for Apple to incentivize the switch with a cash bonus; we’ve seen this work well with our customers.

If Apple wants to become their customers’ primary financial account, they should make it ridiculously easy for their customers to switch their direct deposits.

- Custom metal debit cards. A breathless public has greeted the arrival of past Apple products: iMac, iPod, iPhone, Apple Watch. Apple has already produced one well-reviewed metal card, so expectations for the design of their new debit card would be high. It’s worth noting that a well-designed physical card punches above its weight in terms of wallet share.

- Mobile wallet integration. This is a bit of a no-brainer. After all, Apple popularized the mobile wallet, a way to securely store accounts and cards in the cloud and use them to pay via a mobile device. So a seamless integration between Apple’s banking suite and Apple Pay is de rigueur.

“Banking makes every single feature we offer more interesting.”

- ACH, wires, and in-network payments. As mentioned above, this may be the single most compelling reason for Apple to get into banking. By leveraging ACH, wires, and book payments (fee-free transfers between accounts held at the same bank), Apple has the potential to become a payments network. Apple could dramatically simplify transfering money to friends, family, or merchants, whether they are other Apple users or not.

- Fee-free ATM access. Because Apple lacks bank branches, they would need to provide fee-free ATM access so that their customers can get cash. Rather than negotiate access agreements with hundreds of regional ATM operators, they would likely prefer to go through a network like Allpoint or MoneyPass.

- Checkbooks & mobile check deposit. Let’s face it: some people still use checks. Rather than leave these customers out in the cold, Apple could offer them the ability to print checkbooks or send checks. By the same token, they would almost certainly enable their customers to deposit checks using their phones.

- Connectivity to financial apps and services. Plaid Exchange is a way for financial institutions to help their customers connect their bank accounts to financial apps and services (e.g., Venmo, Acorns, Coinbase). By integrating with Plaid Exchange, Apple can ensure that their logo pops up when customers are searching for their Apple bank accounts.

Add-on banking features

The following features could help Apple differentiate its offering, increase adoption, and drive engagement:

- Additional financing options. Of all possible banking features, financing options in addition to the Apple Card likely represent the greatest opportunity for new revenue. Because they know so much about their customers—including, now, their cash flow—Apple could offer them personal loans, mortgages, and cash advances that are intelligently underwritten and tailored to their needs.

This is what it might look like to apply for an auto loan in Apple Wallet.

- Multiple accounts per customer. This feature has become increasingly popular among neobanks. Under this model, customers obtain a unique bank account (including a unique account number) for each of their financial goals: for example, one for car repair, one for pets, one for a beach vacation. Whenever they get paid, a set amount of money is automatically swept into each account.

- Cashback rewards. By partnering with banks that qualify for increased interchange fees under the Durbin Amendment, Apple could generate revenues of up to 1.5% on each debit-card transaction. As a way to drive adoption, they could use those revenues to pay for attractive cashback rewards on debit-card purchases. They could also fund higher cashback rewards directly or via an affiliate program.

- On-demand virtual debit cards. Virtual debit cards enable customers to make purchases more privately. They can also be programmed with rules about what spend is allowable: how much, to whom, in what geographic location, etc. Imagine, with just a few taps, creating an on-demand virtual debit card for your Hulu subscription. Want to cancel? It’s as easy as deleting the card.

With just a few taps, a user could create a virtual debit card and start making purchases online.

- Personalized recommendations. By leveraging artificial intelligence and machine learning and the trust it’s built with users, Apple could generate high-quality recommendations—and not just better budgets. Imagine the following prompts in your Wallet app: “We saw you looking at this car. Want to finance it?” “You haven’t used this subscription in a while. Shall I cancel it?” “Congrats on your recent raise! To celebrate, here’s a discount on a Macbook.” “Can’t you write this off on your taxes?” “I saw you spent $200 on entertainment. Want a free trial of Apple TV+?” “It looks like you could save this amount today. Shall I put it in your Rainy Day Fund?”.

- Earned income access. Why do we have to wait two weeks to get paid? It’s one of life’s persistent mysteries—as well as an opportunity for innovative companies to set themselves apart. Neobanks like Chime and Varo have built a reputation on making paychecks available to their customers two days early. Companies like PayActiv and Immediate take things one step further, allowing their customers to access a portion of their next paycheck on demand. Apple could develop their own capabilities, offering early paycheck access or on-demand earned wage access.

How Apple will power their banking features: 5 predictions

There are many ways Apple could launch the features listed above. They vary widely in terms of inputs required, time to market, and economics.

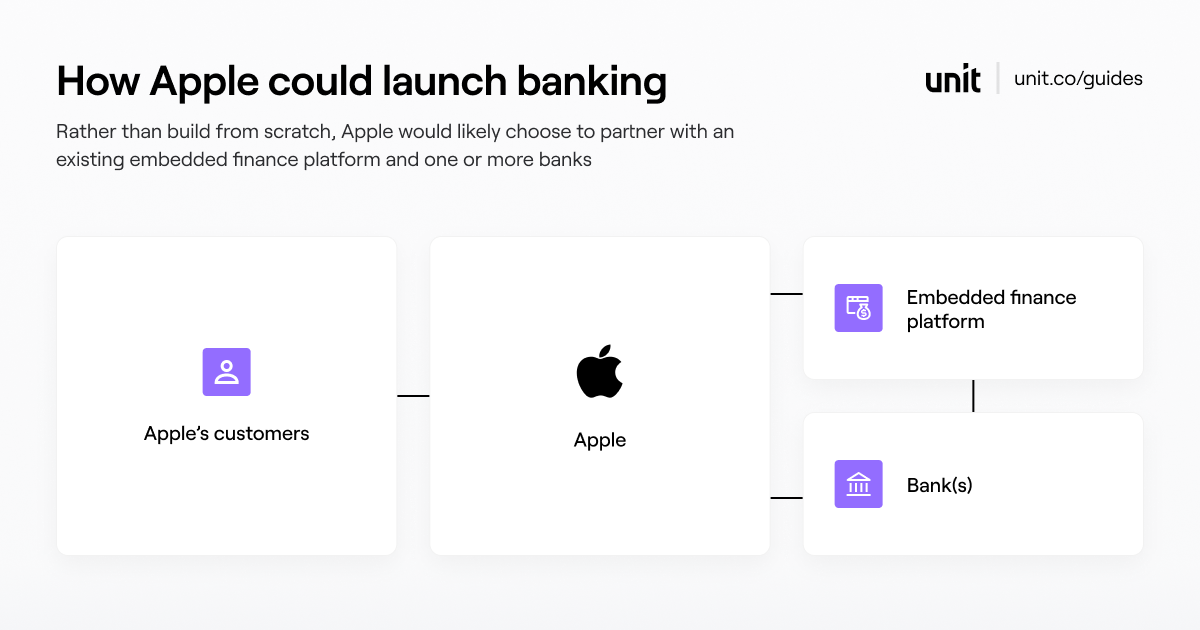

For example, Apple could try to follow in Varo’s footsteps, investing five years and $5M to obtain a national bank charter. They could work with a bank without a platform, as Uber and Lyft did. That would take about two years and $2M. Finally, they could work with an embedded finance platform to partner directly with a bank. Even within that framework, there would still be important decisions to make. Below are five predictions about Apple’s path to launching banking features.

Apple would likely choose to partner with an existing platform rather than build its own banking infrastructure.

- Apple won’t seek a bank charter. Although this might, at first, appear to be an attractive option, it’s actually not viable in the US. In order to become a bank or a bank holding company, Apple would legally be required to limit its activities to banking and closely related activities, which wouldn’t be consistent with its core business.

- Apple will choose to partner with an existing platform rather than build its own banking infrastructure. Companies like Uber, Lyft, and Chime built their own banking backend—largely because, at the time, there weren’t any other options. But we predict that Apple would take a different path. Rather than build technology like ledgers, KYC, AML, transaction monitoring, interest calculations, bank statements, and payment integrations—outside their core competencies—Apple would choose to partner with an existing embedded finance platform. This would significantly improve their speed to market, and it would drastically reduce the size of the banking and compliance teams they would need to hire.

Partnering with an embedded finance platform would significantly improve Apple's speed to market, and it would drastically reduce the size of the banking and compliance teams they would need to hire.

- Apple won’t rely on legacy banking infrastructure. At first glance, it can be hard to tell the difference between embedded finance platforms. But many rely on core banking technologies that were built in the 1980s or 90s. Their infrastructure is brittle, breaks often, and is impossible to configure; it severely limits the kinds of financial products—not to mention, speed of execution—that companies like Apple could offer.

- Apple will choose to work with multiple bank partners. As we outline in our recent blog post, working with multiple bank partners enables you to go to market faster, offer a more complete set of financial products, negotiate better terms, and avoid latency issues. Also, so as to avoid having any one of its bank partners’ balance sheets increase beyond $10B (see our next bullet point), Apple would require a stable of banks across which to spread their customers’ deposits and loans.

- Apple’s bank partners will be small enough to qualify for increased interchange fees under the Durbin Amendment. This one is pure economics. If you’re a bank with assets under $10B, you earn more money on each debit-card transaction. That applies to your partners as well—in this case, Apple. To maximize the revenue they’d earn on interchange, Apple would likely choose to work with a stable of smaller, fintech-oriented bank partners.

This opportunity doesn’t just apply to Apple

With its new banking suite, Apple has the opportunity to change the face of personal finance—and they’re not the only ones.

We’re in the early stages of a paradigm shift in the way financial services are offered to individuals and businesses. In the past, banking was something you did inside a big stone building. Increasingly, it’s something that happens on your phone. In the future, financial services will be hyper-personalized and offered in context—think Affirm at checkout or an on-the-spot payroll advance from Brigit.

We’re in the early stages of a paradigm shift in the way financial services are offered to individuals and businesses.

Perhaps you’re one of the thousands of innovative companies that have been building relentlessly for a specific audience. You’ve earned your customers’ trust; you’re getting to know them in every sense of the word. Their mindset, their problems, their behavior. Now you have an opportunity to become even more valuable to them by helping them manage their money. In the past, such an undertaking would have required years and millions. Now you can do it in a matter of weeks, without hiring a large banking team.

Ready to build financial features into your product? Feel free to drop us a line.